On Saturday, April 11, 2020, COVID-19 Emergency Response Act No.2 received royal assent and the Canada Emergency Wage Subsidy (CEWS) became law.

The main changes to CEWS made during the passage through Parliament were as follows:

- change in the definition of an eligible employee to an individual employed in Canada by an eligible entity in the eligibility period, other than an individual who is without remuneration by the eligible entity in respect of 14 or more consecutive days within the eligibility period i.e., from March 15 to April 11, from April 12 to May 9, or from May 10 to June 6.

- introduction of a 100% refund for employer-paid contributions to Employment Insurance, Canada Pension Plan and Quebec Parental Insurance Plan for each week throughout (not a portion of a week) which an employee is on leave with pay but does not perform any work for the employer, and for which the employer is eligible to claim the CEWS for that employee

The Finance Minister indicated that employers will be able to apply for the CEWS through the Canada Revenue Agency’s My Business Account portal in the next two to five weeks, but hoped that the CEWS will be activated sooner rather than later.

While the CEWS has been brought into effect, further changes are expected to the CEWS and the Canada Emergency Response Benefit, such as:

- to help people who have not lost jobs but are working reduced hours, such as 10 hours or less per week;

- those who are working and earn less than the CERB of $500 per week;

- creating a process to allow individuals rehired by their employer during the same eligibility period to cancel their CERB claim and repay that amount; and

- details about the application process

CEWS – what it is and how it is calculated

CEWS is a taxable subsidy payable to most employers (other than public bodies) whose revenue has declined as a result of COVID-19.

The subsidy is payable at a rate of 75% on salaries or wages actually paid to eligible employees (as defined above) during the period from March 15 to June 6, 2020, up to the first $58,700 normally earned by employees, or $847 per week.

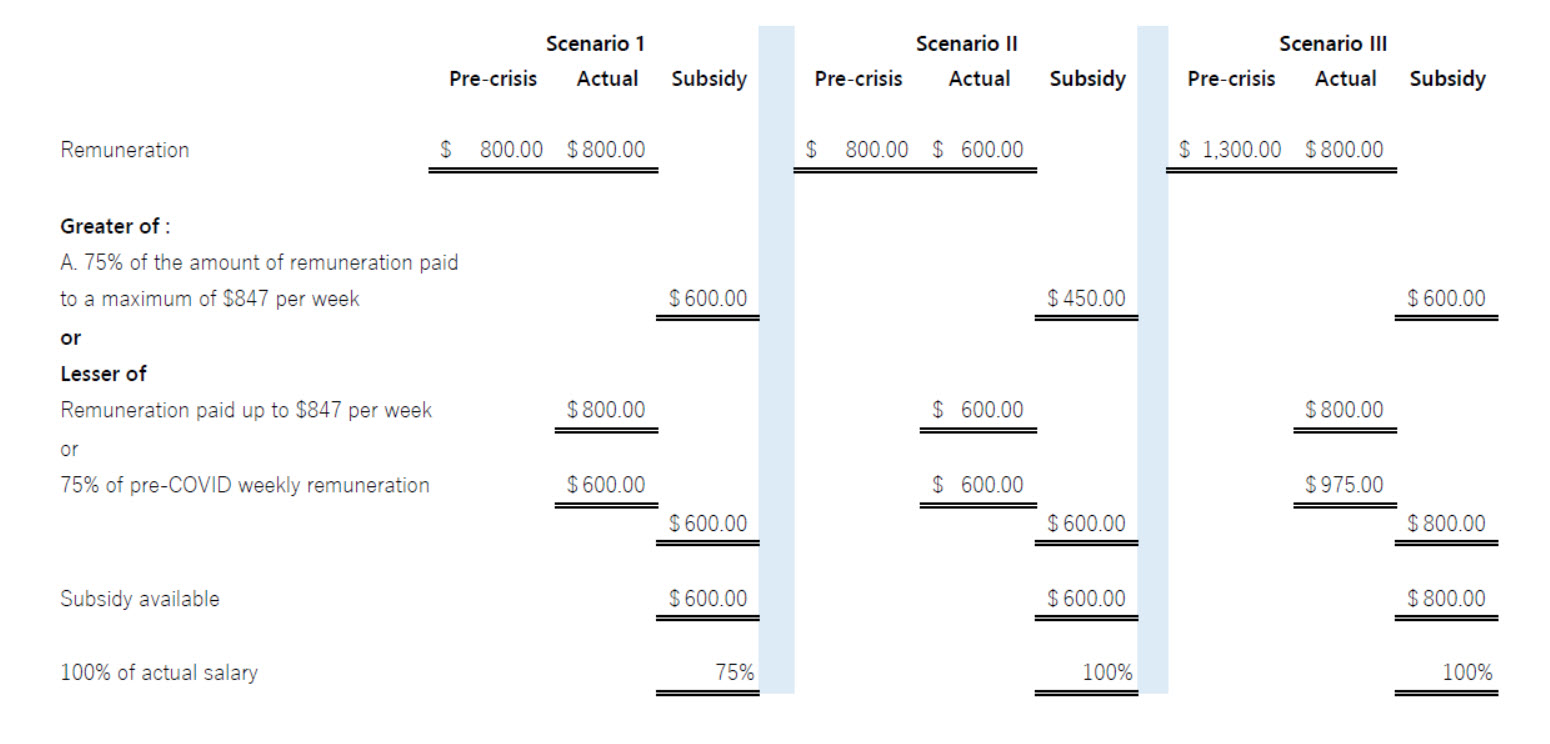

The subsidy is the greater of:

- 75% of the amount of eligible remuneration paid, up to a maximum benefit of $847 per week; and

- the lesser of:

(a) amount of eligible remuneration paid, up to a maximum benefit of $847 per week; or

(b) 75% of the employee’s pre-crisis weekly remuneration, whichever is less.

The following provides an example of how the subsidy is calculated under three scenarios:

Under this formula, some employers may be eligible for a subsidy of up to 100% of the first 75% of pre-crisis wages or salaries of existing employees.

Pre-crisis remuneration for a given employee is based on the average weekly remuneration paid between January 1 and March 15 inclusively, excluding any seven-day periods in respect of which the employee did not receive remuneration.

Eligible remuneration may include salary, wages, and other remuneration like taxable benefits. These are amounts for which employers are generally required to withhold or deduct amounts to remit to the Receiver General on account of the employee’s income tax obligation. However, it does not include severance pay, or items such as stock option benefits or the personal use of a corporate vehicle.

A special rule applies to employees that do not deal at arm’s length with the employer. The subsidy amount for such employees is limited to the eligible remuneration paid in any pay period between March 15 and June 6, 2020, up to a maximum benefit of the lesser of $847 per week and 75% of the employee’s pre-crisis weekly remuneration. The subsidy is only available in respect to non-arm’s length employees employed prior to March 15, 2020.

There is no overall limit on the subsidy amount that an eligible employer may claim.

Any benefit from the 10% Temporary Emergency Wage Subsidy will generally reduce the amount available to be claimed under the CEWS in the same period.

Eligibility for CEWS

Eligibility for the CEWS is determined by the change in the employer’s monthly revenues, calculated for the eligible periods as follows:

| Claiming period | Required reduction in revenue | Reference period for eligibility |

|---|---|---|

| Period 1 March 15 to April 11 | 15% | March 2020 over: • March 2019 or • Average of January and February 2020 |

| Period 2 April 12 to May 9 | 30% | Eligible for Period 1 or April 2020 over: • April 2019 or • Average of January and February 2020 |

| Period 3 May 10 to June 6 | 20% | Eligible for Period 2 or May 2020 over: • May 2019 or • Average of January and February 2020 |

An employer’s revenue for this purpose is its revenue in Canada earned from arm’s-length sources and excludes revenues from extraordinary items and amounts on account of capital.

Employers are allowed to calculate their revenues under the accrual method or the cash method, but not a combination of both. Employers select an accounting method when first applying for the CEWS and are required to use that method for the entire duration of the program.

For registered charities and non-profit organizations, the calculation includes most forms of revenue, excluding revenues from non-arm’s length persons. These organizations are allowed to choose whether or not to include revenue from government sources as part of the calculation. Once chosen, the same approach applies throughout the program period.

Employers are expected, but are not required, to make their best effort to top-up employees’ salaries to bring them to pre-crisis levels.

Refund for Certain Payroll Contributions

Certain employers can claim a 100% refund for certain employer-paid contributions to Employment Insurance, the Canada Pension Plan, the Quebec Pension Plan, and the Quebec Parental Insurance Plan.

This refund is not subject to the weekly maximum benefit per employee of $847 that an eligible employer may claim in respect of the CEWS. There is no overall limit on the refund amount that an eligible employer may claim.

For greater certainty, employers are required to continue to collect and remit employer and employee contributions to each program as usual. Eligible employers apply for a refund, as described above, at the same time that they apply for the CEWS.

Record-keeping and compliance

- employers will need to keep records demonstrating their reduction in arm’s-length revenues and remuneration paid to employees.

- the individual responsible for the financial affairs of an employer will be required to attest to the decline in revenue.

- the employer is required to repay amounts paid under the CEWS if they do not meet the eligibility requirements.

- penalties may apply in cases of fraudulent claims. The penalties may include fines or even imprisonment. In addition, anti-abuse rules will be put in place to ensure that the subsidy is not inappropriately obtained and to help ensure that employees are paid the amounts they are owed.

- employers that engage in artificial transactions to reduce revenue for the purpose of claiming the CEWS will be subject to a penalty equal to 25% of the value of the subsidy claimed, in addition to the requirement to repay in full the subsidy that was improperly claimed.